Stacking with Cross-Validation

Stacking with Cross-Validation (also known as Stacked Generalization) is the traditional and most robust variant of stacking ensemble methods. It uses K-fold cross-validation to generate out-of-fold predictions for training the meta-model, ensuring that every data point in the training set contributes to both base model training and meta-model training. This approach maximizes data efficiency while maintaining proper separation between training and validation to prevent overfitting.

Overview

In cross-validation stacking, the training process leverages the full training dataset through a systematic K-fold cross-validation strategy:

- Training Set: Split into K folds for cross-validation

- Test Set: Reserved exclusively for final evaluation (never seen during training)

- Out-of-Fold Predictions: Generated for the entire training set through CV iterations

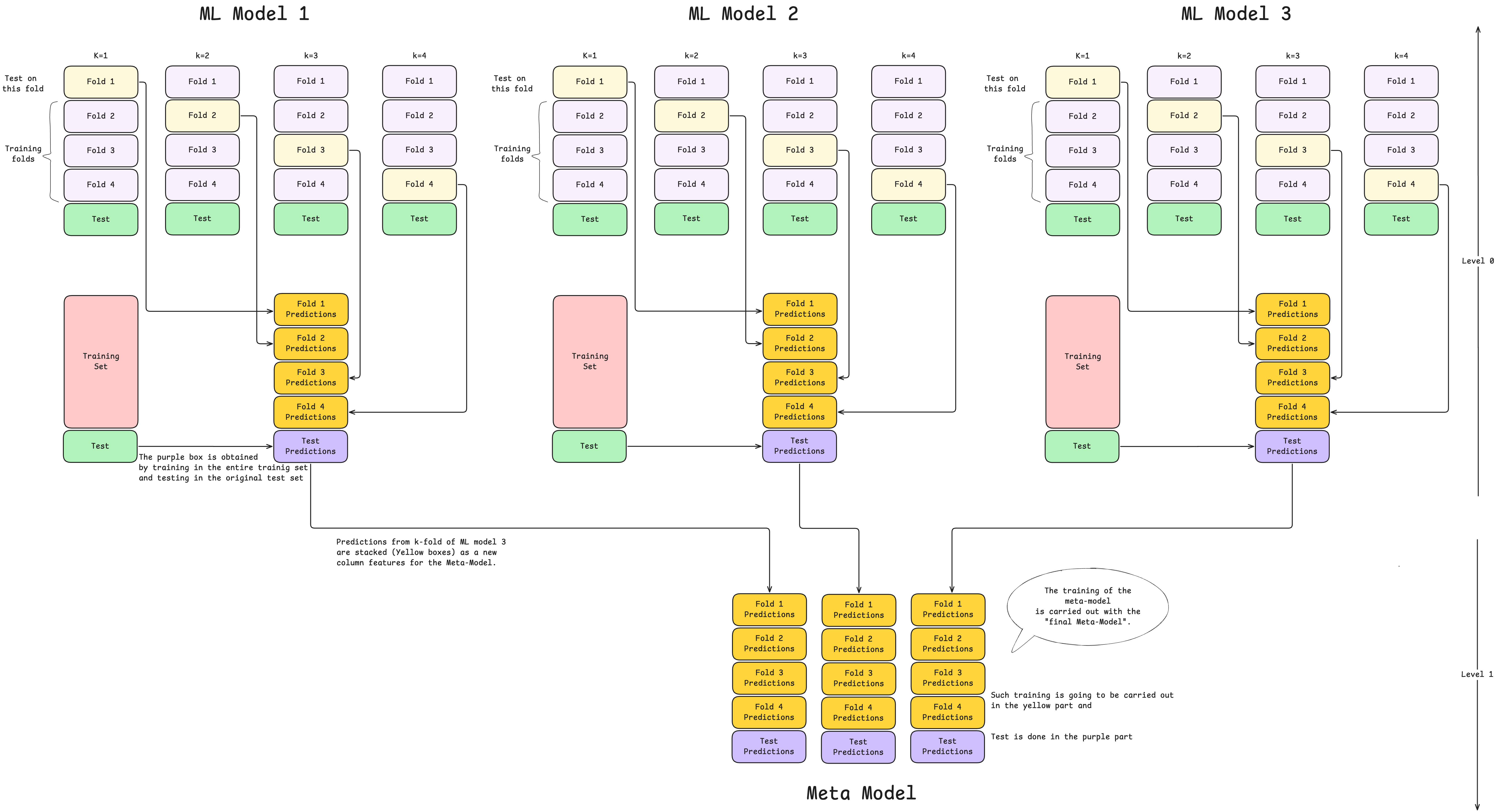

The key distinction from blending is that cross-validation stacking uses all training data efficiently—each sample appears in a validation fold exactly once, ensuring the meta-model learns from predictions on the complete training set.

Diagrammatic Workflow

Implementation Process

Level 0: Base Model Development with Cross-Validation

Step 1: Initial Data Partitioning

Split the main dataset into a training set (typically 80%) and a test set (remaining 20%). The test set is held out completely and used only for final performance evaluation.

Step 2: Set Up K-Fold Cross-Validation

Divide the training set into K equal-sized folds (commonly K=5 or K=10). For classification tasks, use 👉 stratified K-fold to maintain class distribution across folds.

Example with K=5:

- Fold 1, 2, 3, 4, 5 (each containing 20% of training data)

Step 3: Train Base Models Using Cross-Validation

For each base model (e.g., Random Forest, XGBoost, Neural Network):

Iteration 1:

- Train on Folds 2, 3, 4, 5 (80% of data)

- Predict on Fold 1 (20% holdout)

Iteration 2:

- Train on Folds 1, 3, 4, 5 (80% of data)

- Predict on Fold 2 (20% holdout)

Continue until Iteration K:

- Train on Folds 1, 2, ..., K-1

- Predict on Fold K

After K iterations, you have out-of-fold predictions for every sample in the training set. Each prediction is truly out-of-sample since it comes from a model that never saw that particular data point during training.

graph TB

A[Training Data Split into Folds] --> B1[Fold 1 held out]

A --> B2[Fold 2 held out]

A --> B3[Fold 3 held out]

B1 --> C1[Train on other folds]

B2 --> C2[Train on other folds]

B3 --> C3[Train on other folds]

C1 --> D1[Predict on held-out fold]

C2 --> D2[Predict on held-out fold]

C3 --> D3[Predict on held-out fold]

D1 --> E[Combine all OOF predictions]

D2 --> E

D3 --> E

E --> F[Train Meta-Model]

F --> G[Properly Generalized Model]

style G fill:#ccffccStep 4: Generate Test Set Predictions

For each base model, train a final version on the entire training set (all K folds combined). Then generate predictions on the test set. These will be used later for final evaluation.

Note: Some implementations average predictions from all K fold-trained models instead of training a final model on all data. Both approaches are valid.

Level 1: Meta-Model Training

Step 5: Construct Meta-Training Dataset

Compile the out-of-fold predictions from Step 3 into a new dataset where:

- Each column represents predictions from one base model.

- Each row corresponds to one sample from the original training set

- With 3 base models, you'll have a 3-column dataset with the same number of rows as the training set

Key Advantage: Unlike blending, you now have meta-features for 100% of your training data, not just a holdout subset.

Note: Traditional stacking typically uses only base model predictions as features. However, some advanced implementations (stacking with original features) may concatenate the original features with base predictions to give the meta-model more information.

Step 6: Train the Meta-Model

Fit the meta-model (Level 1 learner) using:

- Input features: Out-of-fold predictions from all base models (Step 5)

- Target values: Original labels from the training set

The meta-model learns the optimal strategy to combine base model predictions. It essentially learns which models to trust under which circumstances and how to weight their contributions.

Common meta-model choices:

- Logistic Regression (for classification)

- Linear Regression (for regression tasks)

- Ridge or Lasso Regression (with regularization)

- Gradient Boosting (for complex combination strategies)

- Neural Networks (for highly non-linear combinations)

Final Phase: Inference and Evaluation

Step 7: Generate Meta-Features for Test Set

Use the test set predictions generated in Step 4 as input to the meta-model. These predictions serve as meta-features, structured identically to the meta-training dataset (one column per base model).

Step 8: Generate Final Predictions

Feed the test set meta-features into the trained meta-model. The meta-model applies its learned combination strategy to produce the final ensemble predictions.

Important: No training occurs at this stage. The meta-model simply uses its learned weights and logic to combine the base model outputs.

Step 9: Evaluate Performance

Compare the final ensemble predictions against the actual test set labels to calculate comprehensive performance metrics:

- Classification: Accuracy, Precision, Recall, F1-score, ROC-AUC

- Regression: RMSE, MAE, R², MAPE

Key Differences: Cross-Validation Stacking vs. Blending

| Aspect | CV Stacking | Blending |

|---|---|---|

| Validation Strategy | K-fold cross-validation | Single holdout split |

| Data Usage | Highly efficient (all data used) | Less efficient (holdout unused by base models) |

| Computation Time | Slower (K training rounds per model) | Faster (single split) |

| Meta-Model Training Data | Full training set (out-of-fold predictions) | Smaller (only holdout set) |

| Robustness | More robust (averaged over K folds) | More variance (single split dependent) |

| Complexity | More complex to implement | Simpler implementation |

Advantages

- Maximum Data Efficiency: Every sample in the training set contributes to both base model training and meta-model training, ensuring no data is wasted

- Robust Out-of-Sample Predictions: Out-of-fold predictions provide genuine unseen predictions for the entire training set, reducing overfitting risk

- Better Generalization: The meta-model trains on a larger and more representative dataset, leading to improved performance

- Reduced Variance: Cross-validation averages out the randomness of any single split, producing more stable and reliable results

- Optimal for Small/Medium Datasets: Makes the most of limited data by using every sample efficiently

Limitations

- Computational Cost: Requires training each base model K times, which can be expensive with large datasets or complex models

- Implementation Complexity: More intricate to code and debug compared to simple holdout validation

- Time-Intensive: Training time increases linearly with K, making it slower for rapid prototyping

- Memory Requirements: Storing K models (or their predictions) requires more memory

- Longer Development Cycle: Iteration and experimentation take longer due to extended training times

When to Use Cross-Validation Stacking

Best suited for:

- Small to medium-sized datasets where data efficiency is paramount

- Projects where maximum predictive performance is the primary goal

- Research settings where computational time is less critical

- Competitions where squeezing out every bit of performance matters

- Scenarios with sufficient computational resources

Avoid when:

- Working with very large datasets where computation time is prohibitive

- Quick prototyping or time-sensitive deployments are required

- Computational resources are severely limited

- Simple blending would provide nearly equivalent performance with much less cost

Practical Tips

-

Choose K Wisely:

- K=5 or K=10 are standard choices

- Smaller K (3-5): Faster, less variance reduction

- Larger K (10-20): Slower, more robust, but diminishing returns beyond K=10

-

Stratified Folds:

- Always use stratified K-fold for classification to maintain class proportions

- Particularly critical for imbalanced datasets

-

Model Diversity:

- Combine different algorithm families (tree-based, linear, neural networks)

- Use models with different strengths and weaknesses

- Diversity drives ensemble performance gains

-

Base Model Quality:

- Tune base models individually before stacking

- Poorly performing base models add noise rather than value

- Balance between model diversity and individual quality

-

Meta-Model Selection:

- Start with simple models (Logistic/Linear Regression)

- Only use complex meta-models if simple ones underperform

- Risk of overfitting increases with meta-model complexity

-

Feature Considerations:

- Standard approach: Use only base predictions

- Advanced approach: Include original features alongside predictions

- Test both approaches to see what works for your problem

-

Random Seed Management:

- Set random seeds for reproducibility

- Use the same CV splits across all base models for consistency

-

Avoid Data Leakage:

- Never use test set during any training phase

- Ensure preprocessing (scaling, encoding) is done within each CV fold

Common Pitfalls and How to Avoid Them

1. Data Leakage in Preprocessing

Problem: Fitting preprocessors (scalers, encoders) on entire training set before CV

Solution: Fit preprocessors only on training folds within each CV iteration

2. Test Set Contamination

Problem: Accidentally including test set in any training or validation step

Solution: Isolate test set immediately and never touch it until final evaluation

3. Overfitting the Meta-Model

Problem: Using a complex meta-model that memorizes base predictions

Solution: Start simple (linear models) and use regularization

4. Insufficient Base Model Diversity

Problem: Using multiple similar models (e.g., three different tree models)

Solution: Mix algorithm families (trees + linear + neural networks)

5. Ignoring Computational Budget

Problem: Using too many base models or too large K without considering time

Solution: Start small (3-5 models, K=5) and scale only if needed

Comparison with Other Ensemble Methods

| Method | Approach | Complexity | Performance | Use Case |

|---|---|---|---|---|

| **Stacking - CV ** | Meta-learning with CV | High | Excellent | Max performance, sufficient resources |

| Stacking - Blending | Meta-learning with holdout | Medium | Very Good | Large data, time constraints |

| Bagging | Parallel averaging | Low | Good | Variance reduction |

| Boosting | Sequential learning | Medium | Excellent | General purpose |

| Simple Averaging | Unweighted mean | Very Low | Good | Quick baseline |

Real-World Applications

- Credit Risk Modeling: Combining interpretable (linear) and complex (tree-based) models

- Medical Diagnosis: Stacking multiple diagnostic models for improved accuracy

- Demand Forecasting: Combining time series models with ML approaches

- Image Classification: Ensembling multiple neural network architectures

Advanced Variations

- Multi-Layer Stacking: Adding additional levels (Level 2, Level 3) for deeper ensembles

- Stacking with Original Features: Concatenating base predictions with original features

- Dynamic Weighting: Using sample-specific weights in the meta-model

- Feature-Weighted Stacking: Different base models for different feature subsets

- Temporal Stacking: Time-series aware CV strategies for sequential data